TL;DR: Even if your bank balance stays the same, "low" inflation acts like a slow leak. At 2%, your money loses significant buying power every decade. To stay ahead, your money needs to grow faster than the cost of living.

Let’s talk about the "slow leak" in your bank account.

You’ve probably heard on the news that inflation is coming down and everyone sounds relieved. On the surface, inflation of 2% sounds tiny. It’s the kind of number we usually ignore - like a 2% battery warning on your phone or a small tip at a cafe.

But when it comes to your hard-earned savings, 2% isn't small. It's a persistent thief.

The "Chocolate Bar" Test

Imagine you have £1,000 tucked away in a safe today. Now, imagine that today, a fancy chocolate bar costs £1. Your £1,000 can buy you exactly 1,000 bars. Delicious.

If inflation is 2%, it means that next year, that same chocolate bar costs £1.02. It doesn't feel like much, but now your £1,000 can only buy you 980 bars.

Inflation hasn't touched your bank balance—you still see "£1,000" when you log in—but it has effectively "eaten" 20 bars of chocolate.

The Compound headache

The real problem is that inflation doesn't just happen once; it stacks. That 2% happens this year, then 2% on top of that next year, and so on. It’s the "Compound Interest" of staying poor.

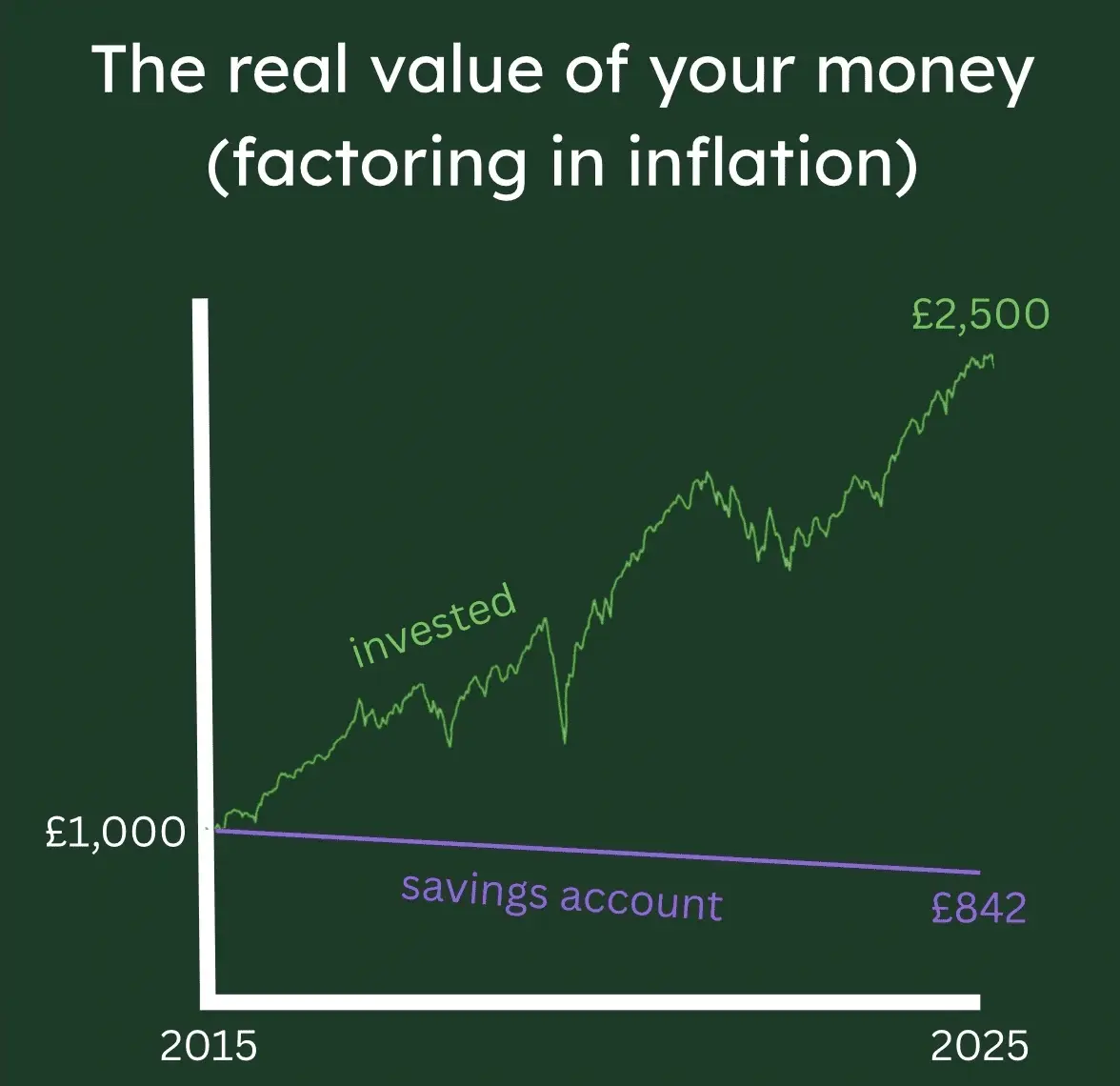

If you leave that £1,000 in a standard savings account for 10 years at 2% inflation, your money doesn't stay the same. In terms of "buying power" (what you can actually get for your money), that £1,000 will feel more like £820.

The Reality: You haven't spent a penny, yet you are effectively £180 poorer.

Why "Safe" is actually risky

Most of us were taught that putting money in the bank is the "safe" thing to do. And for your emergency car repair fund or next month’s rent, the bank is great. It’s secure and easy to reach.

But for your long-term future? The bank is where money goes to slowly lose its value. If your bank is paying you 0.5% interest but prices are rising at 2%, you are literally losing 1.5% of your wealth every single year. It’s like trying to walk up a down-escalator—you’re moving, but you’re still getting lower.

So, what’s the fix?

To beat the "slow leak," you need your money to grow faster than the cost of chocolate (and rent, and fuel). This is where investing comes in.

While the bank gives you a tiny, fixed "thank you" for keeping your money there, investing puts your money to work in the real world—in companies that can raise their prices and grow their profits because of inflation. By owning a piece of those companies (via an index fund), you're on the right side of the equation.

Bottom line: 2% inflation is only a "low" number if your money is growing at 5% or 7%. If your money is just sitting still, that 2% is a 100% guarantee that you’ll be able to afford less tomorrow than you can today.

Not sure how to invest? My jargon-free, engaging and practical course in Bristol will take you from beginner to clicking invest in 2 evenings.